Quarterly Economic Analysis - Q3 2024

Thank you for joining us for our Q3 2024 Economic Analysis at Portafolio Capital.

I recognize that this quarter’s newsletter is being released about a month later than usual. This delay was intentional—we wanted to ensure we accounted for the release of key data over the past several weeks, as well as the FOMC meeting earlier this month.

If you’re reviewing an economic quarter with us for the first time, welcome—it’s great to have you here.

In the insights below, I’ve compiled key data, trends, and commentary that I believe will provide valuable perspective. For those with IRAs or other retirement plans, staying attuned to market movements can help you better visualize and refine your financial goals. Partnering with a trusted investment manager can further strengthen and guide that journey.

Perspectives: Navigating Markets in the Information Age

Over the past 14 years of analyzing domestic financial markets and economic shifts in the U.S., I’ve observed how today’s environment reinforces my perspective on the trajectory of our increasingly globalized economy. As I’ve highlighted in past discussions, the speed of information transmission accelerates economic changes, reshaping markets at an unprecedented pace.

During a recent panel discussion, I was asked whether value still exists in private markets—a question that feels increasingly relevant in today’s technological age. In my opinion, we’ve moved far beyond the concept of privacy in markets, let alone capitalizing on inefficiencies rooted in such premises. Information is now readily available to investors, and the old standard of public disclosure has become less relevant in this era of instant access to data. In a world where information is continuously collected, sourced, and distributed, we must ask ourselves: what role does private equity play in an investor’s portfolio?

In capital management, our fiduciary duty is to assess and manage risk, always acting in our clients’ best interests. The need to steer clear of opaque or poorly understood markets has never been more critical.

Traditionally, private equity thrived by exploiting inefficiencies in undervalued or underperforming companies. However, the rise of real-time data, automated financial analysis, and enhanced regulatory scrutiny has significantly reduced the information asymmetry that once enabled such opportunities. Moreover, the widespread adoption of ESG (Environmental, Social, Governance) metrics and performance benchmarks has added transparency, further narrowing the window for overlooked opportunities.

State of the Markets & Monetary Policy

In a surprising turn of events, corporate earnings have remained strong over the past three consecutive quarters. The Federal Reserve’s 525-basis-point rate hike from March 2022 to June 2023 might, under traditional economic theory, have caused a significant market slowdown. However, the resilience of the consumer has kept corporate earnings robust.

While I believe the Fed is on track to achieve a soft landing, as we head into the new year, I’ll be closely monitoring earnings for any signs of lagging shifts in consumer behavior. Historically, during rate-hiking cycles, sectors like technology and consumer discretionary tend to show weakness, while recession-resilient sectors such as consumer staples and energy outperform. That hasn’t been consistently true in this cycle. Some of our strategies have maintained allocations to both sectors, reflecting a balanced approach.

Most recently, the Federal Reserve pivoted from its hawkish stance, cutting rates by 50 basis points in September and another 25 basis points at its November meeting. The Fed funds rate now sits at a range of 4.5%–4.75%.

This shift underscores the Fed’s confidence in containing inflation, with recent data reflecting cooling price pressures. At the same time, the rate reductions signal a cautious approach to sustaining economic growth, especially given potential slowdowns in consumer spending and corporate investment. While this dovish pivot supports the soft-landing narrative, it also raises questions about emerging risks in labor markets and global demand.

In assessing current market catalysts, it’s clear that the U.S. election outlook has taken center stage. The "Trump trade" has whipsawed markets in recent months, while geopolitical tensions in the Middle East and Ukraine have created an environment where caution is warranted for overseas investments. While some emerging markets, like China, appear attractive due to recent stimulus announcements, the geopolitical risks far outweigh the potential rewards in today’s environment.

The next meeting of the Federal Open Market Committee (FOMC) is scheduled for December 17-18.

Inflation

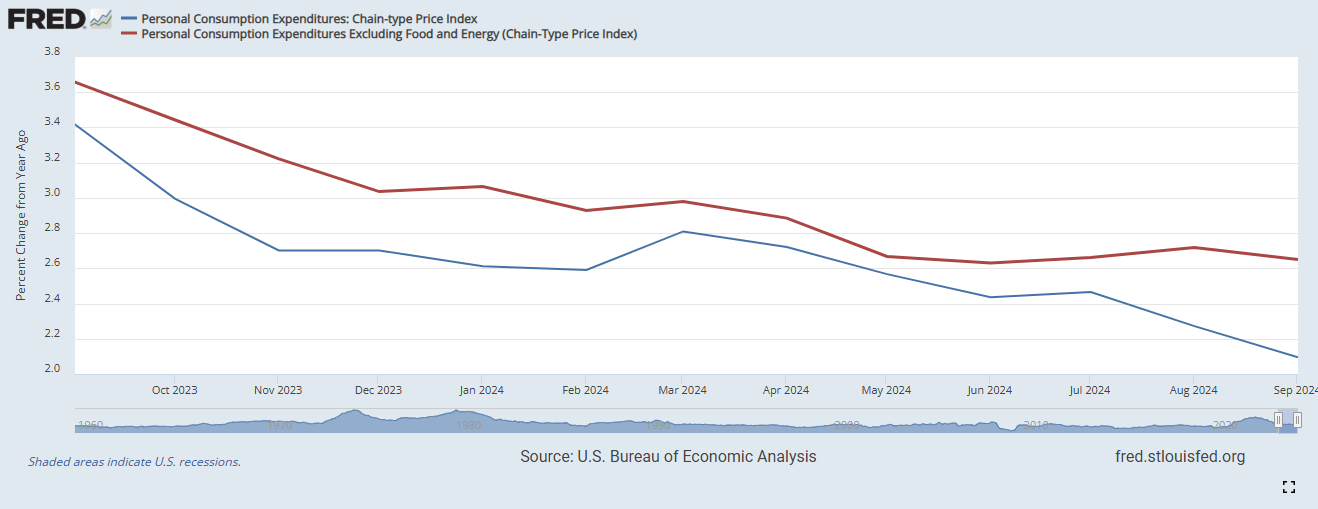

Inflation appears to be under control, as reflected in the latest PCE (Personal Consumption Expenditures) data—the Federal Reserve’s preferred measure. This trend bodes well for monetary policy and market stability, though ongoing vigilance is essential, particularly regarding evolving energy prices.

The PCE price index has shown consistent improvement, falling from its peak annual rate of 6.8% in June 2022. In September, the index rose by 0.2% month-over-month. Goods prices declined by 0.1%, while services increased by 0.3%. Food prices climbed by 0.4%, and energy prices dropped by 2.0%.

Year-over-year, the PCE price index increased by 2.1% in September. Goods prices fell 1.2%, while service prices rose 3.7%. Food prices were up 1.2%, and energy prices saw a significant 8.1% decrease. Excluding food and energy, the core PCE index rose 2.7% compared to the previous year. The next release of PCE data is scheduled for November 27.

Jobs & Unemployment

Since the start of the Fed’s inflation-fighting efforts, unemployment has edged up slightly, reaching 4.1% in October.

The unemployment rate, often viewed as a lagging indicator, has increased modestly, prompting deeper examination of its underlying causes. Despite a strong consumer, I suspect this uptick may be driven by displacement due to rising technologies like AI. Businesses are increasingly adopting lean, technology-driven operations, which could contribute to structural unemployment.

At our firm, we are closely monitoring the adoption of AI across sectors to ensure responsible asset allocation decisions. Nevertheless, a higher unemployment rate can help suppress inflationary pressures, which supports the Fed’s soft-landing goals.

The next unemployment rate data release is scheduled for December 6.

Best,

Mauricio Sanchez

Portfolio Manager & CIO

www.portafoliocapital.com/subscribe

Portafolio Capital Management is an independent wealth and capital management firm based in San Antonio, Texas. With over 12 years of combined investment and macro-economic analysis experience, our goal is to instill confidence in our investors through how we view markets and our investment approach. As a Registered Investment Advisor (RIA) and fiduciary, we are held to the highest standard when it comes to managing your money and are bound by law to act solely in your best interest.

—

Learn more about our strategy and management style by scheduling a 15-minute warm meeting at: https://calendly.com/portafoliocapital/15min.

—

At Portafolio Capital Management, we believe that understanding your unique risk tolerance is key to successful investing. Our comprehensive risk analysis tool is designed to assess your financial personality, time horizon, and comfort with risk, empowering you to make decisions that align with your long-term goals.

https://www.portafoliocapital.com/risk-analysis

—

The content provided is for informational purposes only and should not be considered financial, legal, or tax advice. Individuals should consult their financial advisor, tax professional, or legal counsel before making any investment or financial decisions.

Portafolio Capital Management LLC does not recommend the buying or selling of securities through any published content. We strive to provide accurate information sourced from reliable resources such as FRED, Yahoo Finance, CNBC, and company-specific investor websites. However, we cannot guarantee its accuracy and encourage readers to conduct their own due diligence. We disclaim liability for any inaccuracies and are under no obligation to update or revise the information provided.

Portafolio Capital Management LLC, a Registered Investment Adviser based in Texas, complies with all notice filing requirements in states where we conduct business. This communication does not constitute an offer to sell or an invitation to purchase any investments.

For full disclosures, visit www.portafoliocapital.com/disclosures-and-documents.